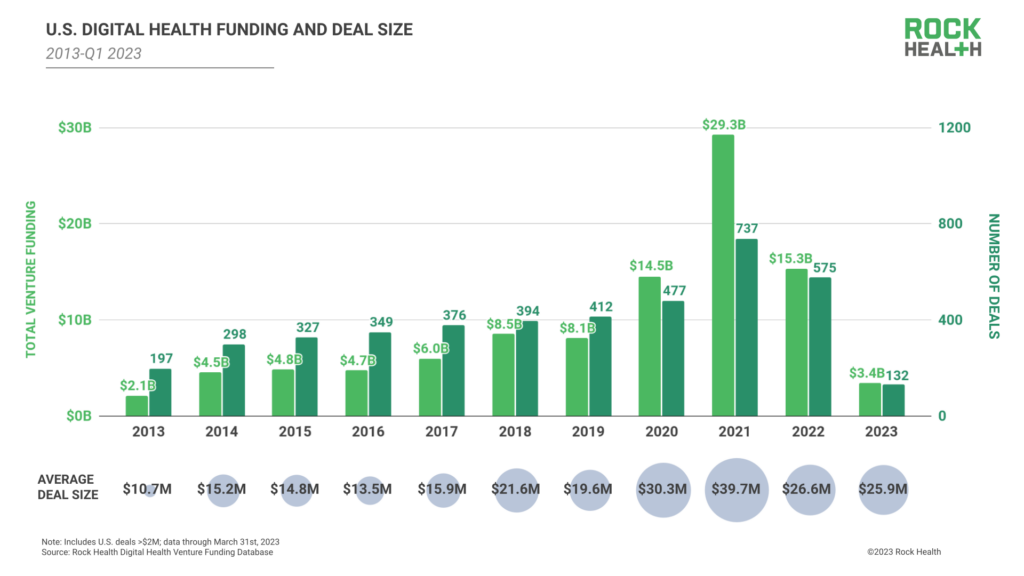

Obviously, the question going into 2023 was whether that trend would continue, or if things would finally start turning around. Now we have our answer, and it's a mix of good and bad: investments were up in the first three months of the year, according to numbers out from Rock Health on Monday, however the situation is more complicated than it seemed to be at the start of the year.

In all, Q1 saw $3.4 billion raised across 132 deals, up 26% from the $2.7 billion raised in Q4, for an average deal size of $25.9 million. Year-to-year, investments are still significantly off from where they had been, going down 43% from $6 billion in Q1 of 2022, while the number of deals fell by 30%.  Q1's $3.4 billion includes six so-called mega deals, aka those that were $100 million or more, matching the combined total of the previous two quarters.

Q1's $3.4 billion includes six so-called mega deals, aka those that were $100 million or more, matching the combined total of the previous two quarters.

Companies that raised mega deals at the start of the year include Monogram Health, a value-based specialty provider of in-home evidence-based care and benefit management services for patients living with polychronic conditions,, which raised $375 million; ShiftKey, a healthcare staffing technology company, which raised $300 million; Paradigm, a healthcare technology company focused on improving access to clinical research for patients, raised $203 milliion; ShiftMed, a company that looks to solve the nursing shortage by offering flexibility and security to nurses, which raised $200 million; Gravie, an employer health benefits company, raised $179 million; and Vytalize Health, a risk-bearing provider enablement platform, raised $100 million.

In total, these six deals alone accounted for 40% of funding in Q1, which the report notes, "signals that the current market is being driven by a select group of large, high impact transactions."

Not out of the woods yet

2022 was a rough year for digital health,

2022 was a rough year for digital health,  Finally, Rock Health also cites the regulatory environment as a pediment to digital health investing, notably the end of the COVID-19 public health emergency at the end of May, which will have a major impact on telehealth companies, especially, while states are begining to undo expanded Medicaid coverage, which will led millions of people to lose benefits.

Finally, Rock Health also cites the regulatory environment as a pediment to digital health investing, notably the end of the COVID-19 public health emergency at the end of May, which will have a major impact on telehealth companies, especially, while states are begining to undo expanded Medicaid coverage, which will led millions of people to lose benefits.  Steven Loeb

Steven Loeb