We all might have guessed that the deflating bubble in Silicon Valley, mirrored by an ongoing global financial market decline, resulted in weaker venture financings in the fourth quarter of 2015.

But just how much weaker? Weaker most ways you slice it, according to new data (Silicon Valley Venture Capital Survey – Fourth Quarter 2015) published by Fenwick & West this week.

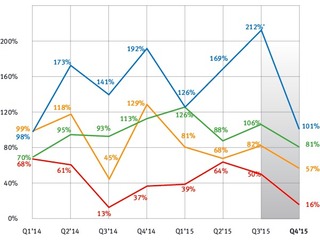

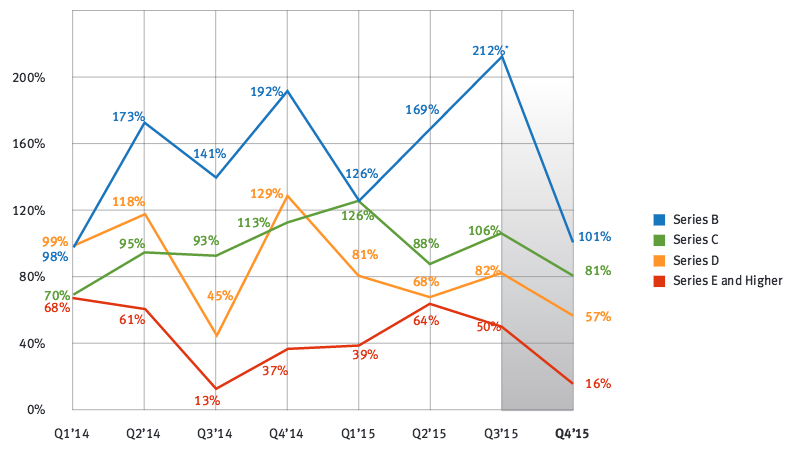

For one, the increase in price of shares between rounds averaged at about 70 percent, which is the lowest it’s been since 4Q 2013. While Fenwick analyzed Series B rounds and later, the most precipitous fall hit the Series B round, as demonstrated in the graph below. So, while in the third quarter share prices increased between the Series A and Series B round by an average of 212 percent, in the fourth quarter prices increased between these two rounds by 101 percent—still strong but significantly lighter.

That was for average percentage price change. Fenwick found similar results when looking at the median percentage price change. In the fourth quarter of 2015, price per share changed by a median 39 percent, less than the 51 percent median change in the third quarter and significantly lower than the 74 percent median change in the second quarter.

When it comes to valuations, the firm compared up rounds (where the company’s valuation is higher than it was in the previous round) against down rounds (where the company’s valuation is lower than it was in the previous round), ultimately providing tangible data around the resetting of sky-high valuations we saw given in 2015.

In the fourth quarter, 82 percent of rounds were up rounds and 12 percent were down rounds, a notable change from the third quarter, when 86 percent of rounds were up rounds and only four percent were down rounds.

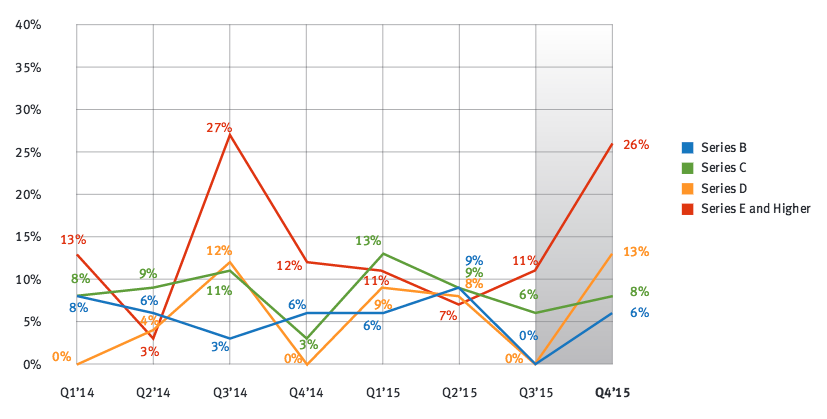

Down rounds increased across all series levels, as demonstrated in the graph below, with the later-stage rounds seeing the biggest jumps. Series E (and higher) down rounds went up by 15 percent and Series D rounds went up by 13 percent, suggesting that some of the biggest culprits for pie-in-the-sky valuations were in these later stage deals.

Interestingly, Fenwick also shared data around percentages of post-Series A financings involving a corporate reorganization, including reverse splits or conversion of shares into another series or classes of shares. In the fourth quarter, eight percent of these rounds involved some form of corporate reorganization, doubling the figure from the quarter previous. The last time it was near that high was seven percent in Q2 2014.