Professional social network LinkedIn posted its third quarter earnings for 2012 Thursday, handily beating Wall Street expectations.

Shares fell slightly in Friday trading, declining 52 cents, or half a percent, to just over $106. But the stock did trade up 8% earlier in the day. And, as you can see from the chart above, shares are still outperforming relative to the other two social media giants that are publicly traded – Facebook and Zynga.

LinkedIn posted late Thursday non-GAAP earnings per share of 22 cents a share and $252 million in revenue. The social network was expected to post earnings of 11 cents per share and $243.9 million in revenue.

The company’s net income was $2.3 million, up from the net loss of $1.6 million it experienced in 2011. Non-GAAP net income for the third quarter was $25.1 million, compared to $6.6 million for the third quarter of 2011.

Adjusted EBITDA for the third quarter was $56.0 million, or 22% of revenue, compared to $24.7 million for the third quarter of 2011, or 18% of revenue.

“LinkedIn had a strong third quarter with all of our key operating and financial metrics showing solid growth,” LinkedIn CEO Jeff Weiner said in a statement. “The last few months mark the most significant period of product development in the company’s history. This accelerated pace of innovation is fundamental to our goal of driving greater engagement on the LinkedIn platform.”

Revenue

LinkedIn saw an 81% increase in revenue, compared to $139.5 million in the third quarter of 2011.

Revenue from Talent Solutions, or what used to be known as Hiring Solutions, accounted for $138.4 million, or 55% of total revenue. It was up 95% year to year.

Marketing Solutions took in $64 million, or 25% of total revenue, up 60% from 2011, when it accounted for 29% of total revenue. Revenue from Premium Subscriptions was up 74% year to year, taking in $49.6 million. It accounted for 20% of the revenue for the third quarter in 2012.

Some $162.4 million, or 64%, of LinkedIn’s revenue came from the U.S., while $89.7 million, or 36%, came from international markets.

“Increased member activity led to sustained growth across our talent, marketing, and premium product lines, resulting in record levels of adjusted EBITDA as well as record operating and free cash flow,” Steve Sordello, CFO of LinkedIn, said in a statement. “We expect a strong finish to the year behind momentum in both our engagement and monetization platforms.”

2012 Outlook

LinkedIn is now projecting revenue for the fourth quarter of 2012 to fall between $270 and $275 million. Adjusted EBITDA is expected to range between $58 and $60 million.

The company has revised its expected revenue range up. In now expects to see full year revenue between $939 to $944 million, up from the prior range of $915 to $925 million. The company has also revised upward its expected adjusted EBITDA range to $202 to $204 million from the prior range of $185 to $190 million.

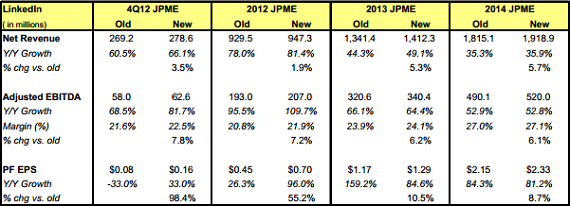

JP Morgan Doug Anmuth is now projecting LinkedIn’s fourth quarter and full 2012 revenue to be even higher than LinkedIn is expecting. He thinks that the next quarter will see revenue of $278.6 million, up from $269.2 million, and full 2012 revenue will hit $947.3 million, up from his previous projection of $929.5 million.

Anmuth outlined what he saw as positives, and negatives, in LinkedIn’s quarterly earnings report.

While LinkedIn added 1.7 million corporate customers during the quarter, engagement is slowing down. he said. The number of unique visitors rose 22% year to year, down from the 38% increase it saw in the second quarter. Page views were up 44%, but had been up 60% in the second quarter year to year.

Anmuth was encouraged that premium subscriptions came in 9% above JP Morgan’s estimates, but noted that challenges internationally, specifically in Europe and India, as well as the impact of China’s slowdown on Australia customers, were hindering growth.

“In our view, LinkedIn is well positioned to take share of both the ~$27 billion addressable worldwide market for staffing and acquisition and the ~$70 billion global online advertising market. We continue to believe LinkedIn is disrupting both the online and offline job recruitment markets, and deeper corporate penetration and increasing member engagement will drive strong results going forward,” Anmuth wrote.

(Image source: http://blog.hubspot.com/)