CrowdHealth deploys a crowdfunding model to pay its users' medical bills

Steven Loeb and Bambi Francisco Roizen speak with Andy Schoonover, CEO and founder of CrowdHealth, a company that deploys a crowdfunding model to pay its users' medical bills.

Our goal is to understand tech breakthroughs radically changing healthcare: the way we screen, diagnose and treat conditions and measure outcomes. And whether tech is helping or hurting our well-being physically and mentally.

Highlights from the interview:

- The origin of CrowdHealth came from when Schoonover’s daughter was having recurring ear infections and needed to get tubes in her ears. When they got the bill it was $8,000 which their insurance company said was medically unnecessary so they refused to pay for it, even though their ear, nose and throat doctor delayed his vacation by a day because he was so worried about her long term potential long term hearing loss. After that the family dropped their insurance and so they started CrowdHealth about two years ago as a way to sidestep having to have insurance.

- 250,000 families every year go bankrupt due to medical events, even though they have health insurance. That is because deductibles, especially Healthcare.gov plans, can be as much as $18,000 for a family. Around 75% of Americans have less than $1,000 in their bank account, so they don't have enough money to pay for that deductible, and that is going to put them into potentially bankruptcy. The second issue that that 18% of claims are denied by health insurance plans, almost one in five. Schooner was fortunate that he can pay an $8,000 bill, but the vast majority of Americans don't have $8,000 sitting in their bank account to pay this type of bill. And so, ultimately, what they're doing is they're either taking on debt, or they're going bankrupt. Both cases are not good situations for these families.

- Studies have shown that people with these high deductible health plans are actually not even going to the doctor are diverting care because they can't afford $15,000 or $18,000. While you would think that people would actually go and maybe they would shop for their services better, because they would look for the lower price, what the studies have shown is, it's just not the case, they're actually putting off care so their healthcare is actually worse than then with low deductible plans.

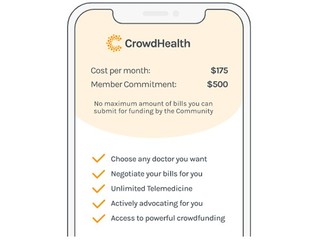

- CrowdHealth costs $175 per person, and the company takes $40 of that as a subscription fee, which is how it makes money, and then the remaining $135 stays in that account and accumulates over time. If somebody in the community has a health event, then the company will reach out and ask its member if they’d be willing to help that other member. For example, if someone broke their arm and it's $5,000, that person would pay the first $500 of that, then CrowdHealth would go and crowdfund $4,500 from 45 people, so $100 each. When someone submits their health funding requests, it actually shows how generous they've been to the community and so there's this reciprocity engine that drives this.

- Doctors will give CrowdHealth somewhere between 30% and 50% discounts if you can pay them in cash on the day of the procedure or the visit. That's why CrowdHwalth’s members can get much better rates than health plans even get, sometimes it's even 70% or 80% less, depending upon what the procedure is. That's ultimately what drives this: it’s enabling people to pay in cash as a consumer, and therefore getting much, much better rates than if the health insurance plan had to pay for it.

- There is something about one human giving generously to another that is powerful. CrowdHealth had a member in Tennessee who had four fingers got cut off in a boating accident, and it was tens of thousands of dollars; when it asked the community to help, the company actually had people reach out and say, “not only do I want to give to her, I want to give more than what you've asked me to give to her." The model connects where their money is going as opposed to a health insurance company that doesn't really care much about them; the money is actually going directly to a person who needs help. The health insurance companies have wedged us in between our neighbors, in between our community, so we're not actually sharing with each other, we're giving it to a health insurance plan who's going to figure out how to allocate those resources. And so, CrowdHealth has seen over and over and over again that people want to help and that people are actually very receptive to giving. It also incentivizes people to go and shop for really good doctors at good prices to not burden the community.

- CrowdHealth’s number one barrier is that it's the devil people know versus the devil they don't. People have struggled with having that behavior change that's required to use CrowdHealth and sometimes saving $5,000 or $10,000 a year is not enough for people to switch over. Fortunately, health plans are some of the company’s best salespeople because you hear these horror stories over and over and over again from health insurance plans declining these claims. It's a ridiculous situation in which we have a healthcare system that's built on a business to business relationship between the hospitals and the insurance companies, and the patients are actually just a cog in the system. People are getting upset about it: health insurance, per Gallup in 2019, was the second most hated industry in America.

- 50% of people get their insurance from their employer, and the other 50% either get it from the government, whether it be Medicaid or Medicare, or they're getting it from on their own. CrowdHealth estimates about 25% to 30% of the population that are getting it on their own, so that's somewhere around 80 million people, and that's the core group of people that is going after. 60% of its customers who sign up were previously uninsured, and 20% to 25% are coming from a corporate health plan because they're so distraught over what their company was giving them such a bad plan that they looked at CrowdHealth as being a better option for them, even though their company was paying for it.

Thank you to our sponsors: Advsr; a boutique M&A advisory firm. They wrote the book on startup M&A called "Magic Box Paradigm: A framework for startup acquisitions." Go to Amazon.com to get your copy. Also thanks to Stratpoint, an outsourced engineering firm and Scrubbed, an online bookkeeping firm. If you need affordable and quality engineering and bookkeeping, check them out. We highly recommend them!

Subscribe to our podcasts to get our interviews and shows as soon as they're published!

Steven Loeb

Steven Loeb